Key numbers

Note: CAGR, or Compound Annual Growth Rate, is a financial metric that

shows the average annual growth rate of an investment or metric over a

specific period (longer than a year) as if it grew at a steady, compounded

rate, smoothing out volatility for better comparison.

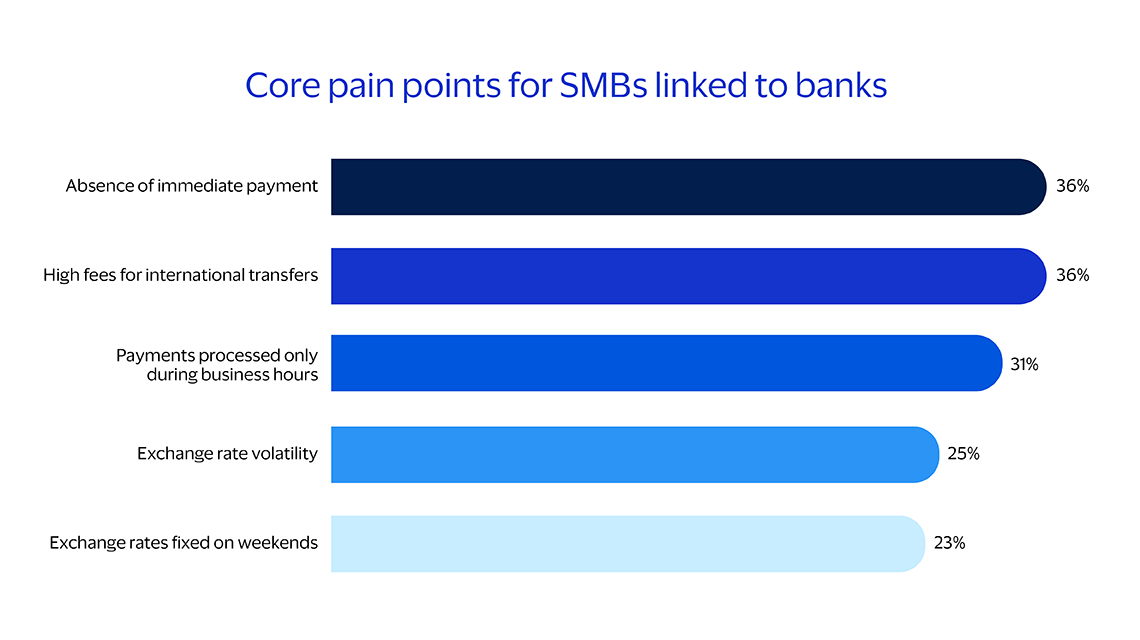

Main pain points for SMBs linked to traditional banks

Source: Visa Consulting & Analytics Survey Analysis.

Three key pillars on which traditional banks should build their Commercial money transfer stronghold

Trust and security

Atomic propositions

Tailored solutions

Conclusion

Banks in CEE face a pivotal moment. With fintechs offering lower fees, faster settlement and seamless digital experiences, the competitive landscape is shifting. But banks retain powerful advantages. By embracing modernisation and client-centric strategies, they can secure relevance in a $2.9 trillion market and turn today's challenges into tomorrow's growth. The time to act is now.

Sources

1. (1) CMS 2024 Market Sizing is based on a combination of data from the 2023 McKinsey Global Payments Map and 2022 EY Visa Direct Global Market Sizing Study (latter based on 2021 data). Russia and China domestic markets are excluded from the global market size. McKinsey Global Payments Map includes 47 markets globally, which comprise ~90% of global GDP. EY Visa Direct Global Market Sizing Study includes 59 markets globally and also estimates the rest of AP, CEMEA, EU, and LAC regions for countries not analyzed specifically.

2. Eurostat. (2025). Statistics Explained: Your guide to European statistics. European Commission. https://ec.europa.eu/eurostat/statistics-explained/SEPDF/cache/6587.pdf

3. VisaNet data analysis, January 2026. Based on card top-ups from Visa active cards to fintech providers in Central Eastern Europe.

Disclaimers

The projections and growth estimates contained in this document are based on historical data, current market trends, and a variety of assumptions. These projections are intended for informational purposes only and should not be interpreted as guarantees of future performance. While we strive to provide accurate and realistic forecasts, numerous factors, including but not limited to market volatility, economic changes, and unforeseen circumstances, can influence actual outcomes. Consequently, there is no assurance that the clients will achieve the projected growth levels. We recommend that clients consider these projections as one of many tools in their decision-making process and consult with Visa Consulting and Analytics for personalised advice.

Case studies, comparisons, statistics, research and recommendations are provided “AS IS” and intended for informational purposes only and should not be relied upon for operational, marketing, legal, technical, tax, financial or other advice. Visa Inc. neither makes any warranty or representation as to the completeness or accuracy of the information within this document, nor assumes any liability or responsibility that may result from reliance on such information. The information contained herein is not intended as investment or legal advice, and readers are encouraged to seek the advice of a competent professional where such advice is required. When implementing any new strategy or practice, you should consult with your legal counsel to determine what laws and regulations may apply to your specific circumstances. The actual costs, savings and benefits of any recommendations, programs or “best practices” may vary based upon your specific business needs and program requirements. By their nature, recommendations are not guarantees of future performance or results and are subject to risks, uncertainties and assumptions that are difficult to predict or quantify. All brand names, logos and/or trademarks are the property of their respective owners, are used for identification purposes only, and do not necessarily imply product endorsement or affiliation with Visa.

This presentation contains forward-looking statements within the meaning of the U.S. Private Securities Litigation Reform Act of 1995 that relate to, among other things, [our future operations, prospects, developments, strategies, business growth and financial outlook]. Forward-looking statements generally are identified by words such as “believes,” “estimates,” “expects,” “intends,” “may,” “projects,” “could,” “should,” “will,” “continue” and other similar expressions. All statements other than statements of historical fact could be forward-looking statements, which speak only as of the date they are made, are not guarantees of future performance and are subject to certain risks, uncertainties and other factors, many of which are beyond our control and are difficult to predict. We describe risks and uncertainties that could cause actual results to differ materially from those expressed in, or implied by, any of these forward-looking statements in our filings with the SEC. Except as required by law, we do not intend to update or revise any forward-looking statements as a result of new information, future events or otherwise.